Apr 23, 2024

Apr 23, 2024

Jointly written with Tushar Kanti Chatterjee (Project & Management Consultant to SK Birla Group)

Oil refineries, being multi-product firms in the classical sense, cannot employ a straight forward cost plus mark-up procedure for computing the prices of their final products. Different quantities of petrol, diesel, kerosene, LPG, as well as other final products are simultaneously produced from a given volume of crude oil and it is not obvious what the crude input content of each product is. Reading between the lines of the Rangarajan Committee and the Parikh Committee reports on oil pricing in India, it is obvious that both were clearly aware of this deep rooted theoretical issue. The Parikh Committee’s recommendation that international oil prices should ultimately guide price fixation in India may have been partly motivated by this factor, though it justified its recommendations instead with reference to the unsustainable fiscal deficit of the Central Government. The prices of petrol, diesel, kerosene and LPG, the four most sensitive of oil products in India, have mostly been administered by the government. Since these prices rarely sync with international prices, the administered prices of some of the products fall short of world market prices while those of others exceed them and, according to the government and public sector oil companies, these distortions lead to avoidable fiscal deficits for the government.

Oil refineries, being multi-product firms in the classical sense, cannot employ a straight forward cost plus mark-up procedure for computing the prices of their final products. Different quantities of petrol, diesel, kerosene, LPG, as well as other final products are simultaneously produced from a given volume of crude oil and it is not obvious what the crude input content of each product is. Reading between the lines of the Rangarajan Committee and the Parikh Committee reports on oil pricing in India, it is obvious that both were clearly aware of this deep rooted theoretical issue. The Parikh Committee’s recommendation that international oil prices should ultimately guide price fixation in India may have been partly motivated by this factor, though it justified its recommendations instead with reference to the unsustainable fiscal deficit of the Central Government. The prices of petrol, diesel, kerosene and LPG, the four most sensitive of oil products in India, have mostly been administered by the government. Since these prices rarely sync with international prices, the administered prices of some of the products fall short of world market prices while those of others exceed them and, according to the government and public sector oil companies, these distortions lead to avoidable fiscal deficits for the government.

The manner in which the prices are administered, as reflected in the price build-up formulae published by IOC, HPCL and BPCL, raises major questions. The so-called “desired” Indian price of these products (except for petrol) are computed by adding to the internationally ruling cargo loading, or free on board (FOB), prices in Gulf countries (1) the import costs (viz. customs duties, ocean freight and port charges), (2) the inland freight-cum-delivery costs and finally (3) the costs and profit margins of Oil Marketing Companies (OMCs) run by IOC, HPCL and BPCL. The “desired” prices arrived at in the process turn out to be too high. Consequently, lower “administered prices” are fixed by the government, thereby generating a shortfall from the desired prices. This shortfall is described as an “under-recovery” for the OMCs, which is claimed to be the raison d’etre for oil sector subsidization.

The procedure adopted for computing the “desired” prices is questionable however, since the final products so priced are mostly produced at home. The above referred costs associated with imports should therefore apply to the imported part of raw material (crude oil) and not to the final outputs produced with its help. The “desired prices” of petro-products in India therefore tend to over-value them. Besides, the subsidy-driven “administered prices” too increase subsequently through the imposition of excise duties, VAT, sales taxes, surcharges etc.

Subsidies are normally in order when the cost of production exceeds the price of the final product, but the idea of “under-recovery” does not concern itself with the cost of production issue at all. Consequently, it is important to try and understand what in fact the cost structure for the critical petroleum products is and then try and calculate its relationship with the revenue generation potential of a rational administered pricing scheme.

Towards this end, we suggest below an elementary framework for pricing the four major petro products. To keep the analysis as simple as possible, we assume further that there are no taxes on crude oil and end up with an estimate of the potential revenue surplus produced by the oil refineries and marketing corporations. The said surplus is then viewed as a possible source of tax revenue for the central and state governments. The proposals will also indicate how the subsidy burden of the Central Government may be eliminated altogether without resorting to excessively high oil price hikes, thereby seriously questioning the wisdom behind the recently promulgated pricing policy for diesel and LPG.

In order to evaluate the annual financial impact of adopting our pricing scheme, we will need actual consumption and other data (such as refinery costs, dealer commissions etc.) to arrive at estimates of costs and revenues. Since data for the financial year 2012-13 is not yet available, we shall apply our price formulae to the data for the year 2011-12 and calculate possible gains that the government and oil companies could have made in that year. Once the complete figures for the year 2012-13 are published, it will be possible to carry out the same exercise for the current year.

The Pricing Scheme

Our primary goal is to adopt a cross-subsidized administered pricing scheme for petrol, diesel, kerosene and domestic LPG. The suggested prices and the motivations underlying them are described below.

Petrol

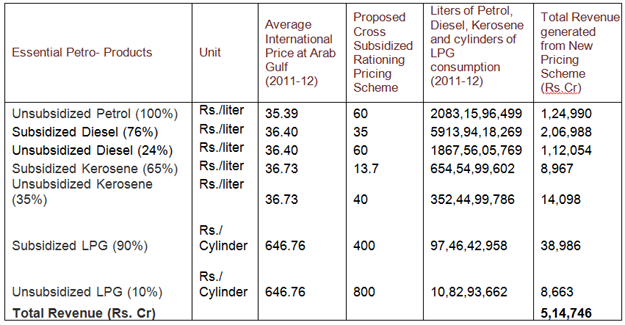

Petrol is largely an item of final consumption. Its price has little impact on inflation through forward linkages. Also, it is mostly consumed by the relatively affluent sections and need not be subsidized. Thus, the price of petrol is fixed higher than the average 2011-12 international price (viz. Rs.35.39 per liter) at Rs. 60 per liter, which still falls short of the 2011-12 average petrol price of Rs. 64.43 in India.

Diesel:

According to the Parikh Committee, the approximate consumption pattern of diesel in India was: Railways -- 6 per cent; trucks --37 per cent; buses -- 13 per cent; taxis -- 8 per cent; agriculture -- 12 per cent; industry --10 per cent; power generation -- 8 per cent; and private cars -- 6 per cent. Thus, the diesel consumption for railways, trucks, buses, taxies and agriculture accounts for about 76 per cent of the total consumption, while that for industry, power generation and private cars constitutes the balance of 24 per cent. In other words, 76 per cent of the diesel consumed is critical in nature and needs to be subsidized. With this consideration in mind, we suggest a diesel price for critical use to be Rs.35 per liter. For the remaining 24 per cent of diesel use, the price is chosen to be Rs. 60 per liter, which matches the suggested price for petrol. (The Parikh Committee report was submitted in Feb, 2010. Consequently, the consumption pattern assumed here may have changed since then. In particular, it is almost certain that diesel use for privately owned cars has shot up.)

A differential pricing formula for diesel may be implemented through the much discussed direct cash transfer procedure. Every truck, taxi, bus and tractor should have a unique number assigned through RFID chips of the sort assigned to current models of vehicles. The petrol pumps will scan the unique number for generating retail shop bills and sell diesel at the same price of Rs.60 per liter to all consumers. However, the drivers/owners of transport vehicles and tractors will receive a subsidy of Rs. (60 - 35) = Rs.25 per liter per month against the deposit of original bills to designated authorities. Similarly, farmers may be allowed to use a maximum of 15 liters of diesel for each bigha watered by diesel pumps and receive a subsidy of Rs.(60 - 35) = Rs.25 per liter per bigha

Kerosene:

Estimates suggest that 35 per cent or more of PDS kerosene is diverted to take advantage of higher market prices. A single price in the market must therefore prevail as in the case of diesel. We suggest this price to be Rs. 40 per liter. The subsidized price of PDS kerosene will be Rs.13.70 per liter for 65 per cent of total kerosene consumption. As with diesel, ration shops could sell it at a uniform price of Rs.40 per liter. The Ration/BPL card holders would need to open bank accounts in nearby nationalized banks. Under this arrangement, they would receive bank transfers of Rs. (40 – 13.7) = Rs.26.30 per liter of kerosene purchased every month. In the absence of branches within a 3 km radius, the Panchayat would be assigned the responsibility of distributing cash subsidy to the villagers and submit the accounts to concerned authority. This should reduce some, though not all, malpractice and lower PDS Kerosene purchase to one third of the observed levels.

LPG:

The Parikh Committee observes that rural households use 6 to 9 cylinders per year (since they also use wood as an alternate fuel), whereas urban and semi-urban households use 9 to 20 cylinders per year, with lower income groups using PDS kerosene as substitute fuel for cooking.

There is a clear need to restrict the availability of subsidized LPG to households. However, the Parikh Committee figures suggest that average urban households consume around 14 cylinders annually, whereas many rural households consume 9 cylinders per year. The supply of subsidized domestic LPG could therefore be rationed to one cylinder per month (i.e. 30 days) for each household (instead of the 6 cylinders per year norm proposed by the government recently). We assume further that around 10 per cent of the population will consume more than 1 cylinder per month (30 days).

The unsubsidized domestic LPG could be priced Rs.800 per cylinder (operative for a second cylinder purchased within 30 days of the last purchase). The subsidized price is fixed at Rs.400 per cylinder. Also, as decided by the government recently, a common data base of subscribers would locate families with multiple LPG connections and their extra connections will then be locked.

The consumption pattern of these 4 essential petroleum products for the year 2011-12, their actual internationally prevailing prices, the suggested rationed prices and the total revenue the latter would generate assuming unchanged consumption rates are presented in Table 1.

Source for Consumption Pattern: Petroleum Planning and Analysis Cell

As the table shows, the total revenue that the 4 essential products would generate in 2011-12 under the suggested price scheme and unchanged consumption equals Rs. 5,14,746 cr.

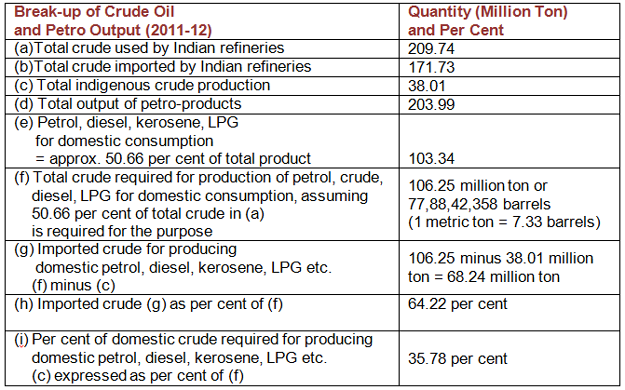

The total crude oil cost of production of petrol, diesel, kerosene and LPG needs to be calculated prior to other costs of production. The total crude oil consumed by Indian refineries in 2011-12 was 209.74 million ton. This broke up into 171.73 million ton of imported crude and 38.01 million ton of domestically extracted crude oil. The total production of petro-products by Indian refineries was 203.99 million ton. Around 50.66 per cent of this total output, or 103.34 million ton consisted of petrol, diesel, kerosene and LPG for Indian consumption. Technology suggests that the same percentage of the total (imported plus domestically produced) Indian mix of crude, or 106.25 million ton (or 77,88,42,358 barrels), was needed to produce the petrol, diesel, kerosene and LPG for Indian consumption. The aggregate quantity of domestic crude produced (38.01 million ton) turns out to be 35.78 per cent of the above calculated total crude need. This leaves a balance of 106.25 million ton minus 38.01 million ton = 68.24 million ton of imports to bridge the shortfall of crude required for the four essential products. The latter equals 66.22 per cent of the total Indian mix of crude used up. The calculations are captured by Table 2.

Source for Production and Consumption Pattern: Petroleum Planning and Analysis Cell

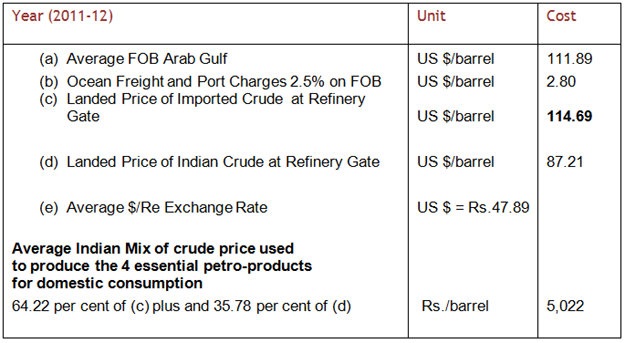

Thus, the average price of a barrel of the Indian mix of crude should be calculated by attaching a weight of 64.22 per cent to the import price and 35.78 per cent to the indigenous price. This calculation is presented in Table 3.

Given that the quantity of Indian mix of crude used to satisfy the domestic need for the four products was 103.34 million ton or 77,88,42,358 barrels, the nominal value of this crude, using the price computed in Table 3, was Rs.3,91,101 cr. The balance amount of imported crude, i.e. (209.74 – 106.25) million ton = 103.49 million ton was used to produce items other than the 4 major products for domestic consumption considered so far. These consisted of Naphtha, ATF, LDO, Lubes, Furnace Oil, LSHS, Bitumen, Asphalt, and other exported petro-products.

Surplus Generated by Suggested Pricing Scheme

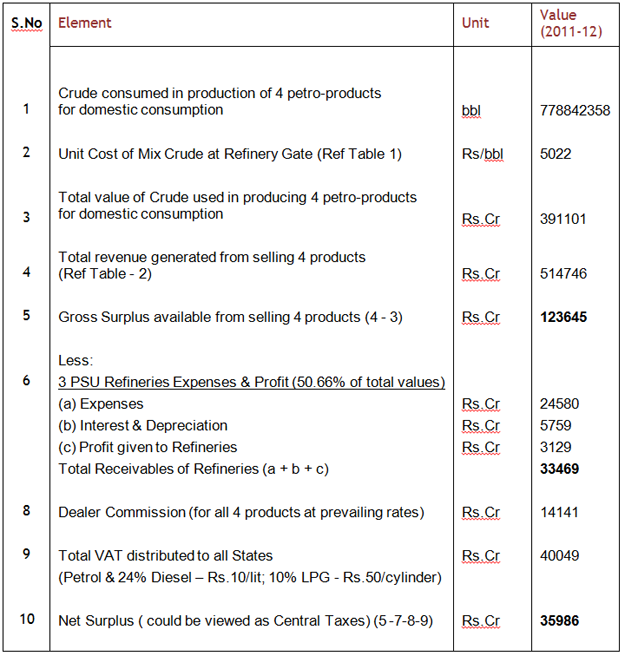

Under the adopted pricing scheme, the gross surplus realized from producing the 4 essential products is then Rs. 5,14,746 - Rs. 3,91,101 cr = Rs. 1,23,645 cr. This gross surplus would need to cover refinery expenses and margins, dealer commissions, VAT as well as Central taxes. As per the information available from the websites of the oil companies, these figures for the year 2011-12 were as follows:

Refinery Expenses:

The total expenses of the refineries were Rs. 48,520 cr. (These included power and fuel cost, employee cost, other manufacturing expenses, selling and administrative expenses and miscellaneous expenses.) Their interest and depreciation charges amounted to Rs.11,369 cr. Assuming as before that 50.66 per cent of the expenditure was incurred in producing the 4 sensitive products, their total production cost amounted to Rs.30,340 cr (approx).

Refinery Margins:The total margin of all 3 refineries was Rs.61,77 cr. Once again, applying the 50.66 per cent argument, the profit derived from the 4 products should have been Rs.3,129 cr (approx).

Dealer Margin:

Based on dealers’ margin for the 4 products prevailing in the very recent past, the total margin turns out to be Rs.14,141 cr.

VAT

In lieu of VAT, we suggest a consumption based tax structure for unsubsidized petrol, diesel and LPG. More precisely, we propose a cess of Rs.10 per liter of petrol consumed, Rs.10 per liter for unsubsidized diesel consumed and Rs.50 per cylinder of unsubsidized LPG. The motivation underlying the suggested tax structure is to leave the prices of the products unaffected and uniform across the country. As opposed to this, taxes (such as VAT) charged as a per cent of the price paid will raise prices above the norms we have adopted. Using the consumption figures in Table 1 then, the total revenue generated by the cess will be Rs.40,049 crs.

After taking account of these three deductions from the gross surplus of Rs. 1,23,645 cr, we are left with a net saving of Rs.35,986 cr. This sum is available in its entirety to the Central Government. Since our approach is based on cross-subsidization of products alone, the Central Government’s subsidy outgo on oil account is not a part of the calculation. This means that the Central Government is relieved of its subsidy burden of Rs. 1,40,000 cr for 2011-12, arising out of the so-called under-recoveries. In addition, it will earn an extra revenue of Rs.35,986 cr from the petroleum sector. This means that instead of sustaining a fiscal loss, the government could have actually gained a sum of Rs. (35,986 + 1,40,000) cr = Rs.1,75,986 cr, which could significantly reduce its fiscal deficit. The above cost calculations have been presented in a tabular form in Table 4 below.

Besides item 6(c) in Table 4, the oil companies earn substantial profits from selling the other petro-products listed earlier, since these are sold at market driven prices. Also, In 2011-12, their net exports of the 4 products were worth Rs.1,45,886 cr. Thus, 6(c) provides a minimum bound on the profits of the oil companies. Similarly, since the Central Government will earn taxes from these other sources as well, item 10 in Table 4 too stands to be augmented to a larger figure.

The analysis indicates then that there is ample scope for generating surplus revenue through a suitable cross-subsidization scheme. It is doubtful therefore that there is no way of reducing the government’s fiscal deficit except through the recently adopted policy of removal of subsidies for the under-privileged masses. The matter calls for serious debate amongst policy makers, technologists and economists. Avoiding such discussions can only add to inflation and reduce our growth rate.

Conclusion

As far as cost saving policies are concerned, it is important to note that a merger of the three PSU refineries will lead to a minimum saving of Rs.10,000 crs by cutting down on excess man-power, particularly at the executive level (to wit, IOC maintains a highly uncompetitive executive to workmen ratio of 1:1.35), as well as operating, capital and overhead expenditures. We expect another 5-10 per cent possible reduction in prices of these 4 products through this channel.

The analysis presented is not entirely fool proof of course. First, it is based on a number of assumptions regarding the relationship between total costs and revenues. More research is required to verify these relationships and assumptions. Also, the exercise needs to be repeated as more data is available for the current financial year. The surplus figures could change in the process, calling thereby for fine tuning prices. To protect the poor, such price changes should be accommodated through upward revisions in the price of petrol, unsubsidized diesel (24 per cent) and unsubsidized LPG (10%) as far as possible. Every 15 days these values should be monitored and the price of petrol, unsubsidized diesel and LPG ought to be adjusted. In other words, the prices suggested should not be treated as rigid in nature. Depending on frequently changing international circumstances, our prices will have to change too.

Secondly, while we have changed the 2011-12 prices to compute the gains, we assumed that the consumption of the products remained unchanged. According to the law of demand, consumption should have been affected by prices and, to that extent, our revenue figures would need to be reconsidered. Of course, the demand for these products being somewhat inelastic in nature, the results arrived at should not be significantly altered. Thirdly, our rationing scheme depends on the success of the direct cash subsidy proposals. So far, the rate of success of these cash transfer schemes is not clear. Finally, our choice of the differential between diesel and kerosene prices appears somewhat large and need not be able to prevent malpractices surrounding contamination of the fuels. This problem exists for the actual price scheme ruling currently in the currently.

A great deal of work then remains to be done, but our approach clearly points out that the government had not looked into enough alternatives before announcing the latest policies. The least one should expect is a white paper from the government clarifying the details of the cost of production for petro-products in India.

08-Oct-2012

More by : Dipankar Dasgupta

|

|

Thank you Kumud-babu. It took me a while to produce this piece. However, Tushar's enthusiasm and research was the driving force that kept me going. I am sure that we will need to work more on the subject and refine our results. Whatever we have done so far points out though that the rationale offered for the current pricing scheme for petro-products in India is not too convincing. |

|

|

Welcome back dear Dipankar. Must thank you for this beautiful analysis of perhaps one of the most topical issues of the day. |